The HDB approval process is the mandatory regulatory procedure governing eligibility verification, application submission, and transaction validation for residential property transactions within Singapore’s public housing system. For both individual buyers and property developers, understanding this process determines whether a transaction proceeds on schedule or stalls due to documentation gaps or missed deadlines. The Housing and Development Board (HDB) administers this process through digital platforms including the HDB Flat Portal and the Resale Portal, with Singpass authentication required at every stage. Key documents such as the HDB Flat Eligibility (HFE) letter, Option to Purchase (OTP), and resale application form the procedural backbone of any approved transaction.

What is the HDB flat eligibility (HFE) letter and why is it required?

The HFE letter is the foundational document in the HDB application process. It consolidates three previously separate documents into one: proof of eligibility to purchase, the maximum HDB Housing Loan amount, and applicable CPF housing grants. No buyer may exercise an Option to Purchase without a valid HFE letter in hand.

The application follows a strict two-step digital workflow through the HDB Flat Portal using Singpass. The first step is a preliminary eligibility assessment, which provides indicative results but does not constitute final approval. The second step is the full submission, which must be completed within 30 days of the preliminary check. Failure to complete the full submission within this window requires the applicant to restart the entire process from the beginning.

Processing time for the HFE letter averages 21 working days, though this can extend during peak periods such as Build-To-Order (BTO) sales launches. Once issued, the letter carries a validity of 6 months, which means applicants who delay their property search risk expiry before they can exercise their OTP.

Common pitfalls at this stage include:

- Allowing the HFE letter to expire before exercising the OTP, requiring a full reapplication

- Failing to complete the full submission within the 30-day window after the preliminary check

- Submitting inaccurate income or financial data, which triggers delays in eligibility confirmation

- Misunderstanding that the preliminary assessment is indicative only and does not confirm loan limits or grant amounts

Pro Tip: Apply for the HFE letter before scheduling property viewings. This positions you to act immediately once a suitable flat is identified, without waiting three to four weeks for processing.

How does the HDB resale flat approval process work step by step?

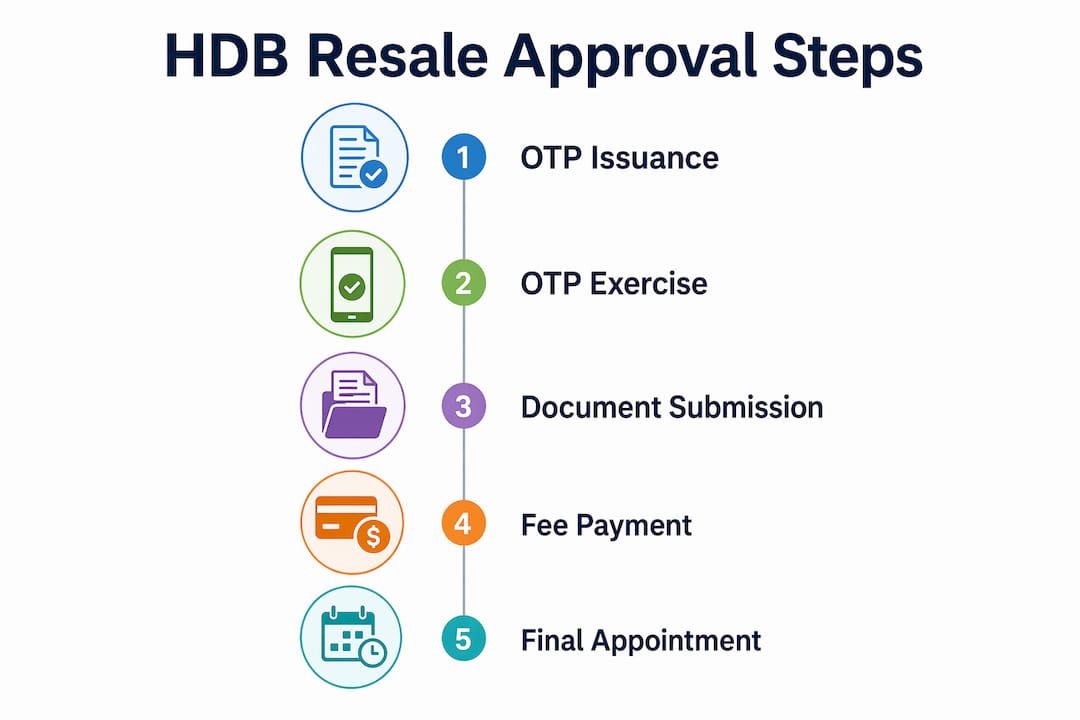

The resale flat approval process follows a defined sequence from OTP issuance to final key handover. Each stage carries specific documentation requirements, payment obligations, and coordination between buyer, seller, and their respective solicitors.

The standard sequence proceeds as follows:

- OTP issuance: The seller grants the buyer an Option to Purchase, accompanied by the option fee payment.

- OTP exercise: The buyer exercises the OTP within the stipulated period and pays the exercise fee.

- Resale portal submission: Both buyer and seller must submit their respective portions of the resale application within 7 days of each other via the HDB Resale Portal.

- Document endorsement: Both parties review and endorse the application documents digitally through the portal.

- Technical flat inspection: HDB conducts a physical inspection of the flat to verify its condition and structural compliance.

- Fee payments: Stamp duties, legal fees, and applicable levies are paid at this stage.

- HDB approval: Following completed endorsement and payment, approval is typically granted within 2 weeks.

- Final appointment at HDB Hub: Both parties attend the completion appointment, where loan disbursements are processed, CPF refunds are issued, and keys are handed over.

The table below summarizes the timeline and required actions at each stage:

| Stage | Typical Duration | Required Action |

|---|---|---|

| OTP issuance to exercise | 1–21 days | Buyer exercises OTP, pays exercise fee |

| Resale portal submission | Within 7 days of each party | Both parties submit applications separately |

| Document endorsement and payment | 1–2 weeks | Digital endorsement, fee settlement |

| HDB approval | Approximately 2 weeks post-endorsement | HDB reviews and issues approval |

| Final appointment and completion | Scheduled by HDB | Loan disbursement, CPF refund, key handover |

| Total process | 8–12 weeks | From OTP exercise to completion |

The total resale completion timeline spans 8–12 weeks from OTP exercise to the final appointment. Most transactions engage HDB-appointed solicitors, with typical legal fees ranging from S$1,200 to S$2,400. Using appointed solicitors reduces coordination risk and keeps the process on schedule.

Pro Tip: Coordinate with your solicitor before submitting the resale application. Misaligned submission dates between buyer and seller are among the most common causes of processing delays.

How does HDB validate eligibility and compliance during approval?

HDB’s portal does not rely on manual review alone. The system performs automatic validations of eligibility and financial compliance at multiple checkpoints throughout the application. This digital verification layer is what allows the process to maintain both speed and regulatory integrity.

The portal cross-checks the following automatically:

- Eligibility status: Citizenship, family nucleus composition, and income ceiling compliance

- Minimum Occupation Period (MOP): Verification that the seller has fulfilled the mandatory occupation period before the flat can be sold

- Additional Buyer’s Stamp Duty (ABSD): Automated checks on existing property ownership to determine applicable stamp duty obligations

- CPF and financial commitments: Cross-referencing CPF account balances, outstanding loans, and grant eligibility against declared financial data

- Property ownership records: Verification that neither buyer nor seller holds disqualifying property interests

Accurate self-declaration is not optional. Discrepancies between declared information and government records trigger application holds, which extend the timeline and may result in outright rejection. The HDB portal’s role extends beyond approvals to serve as a real-time compliance verification system, cross-referencing data from CPF Board, Inland Revenue Authority of Singapore (IRAS), and the Singapore Land Authority (SLA).

Grant schemes such as the CPF Housing Grant, Enhanced CPF Housing Grant (EHG), and Proximity Housing Grant (PHG) each carry specific eligibility conditions. These conditions are verified automatically during the approval stage. Applicants who declare grant eligibility incorrectly face clawback obligations after completion, which creates significant financial and legal complications.

For developers and compliance professionals, understanding the planning approval process for Singapore projects is equally relevant, as HDB’s validation framework intersects with Urban Redevelopment Authority (URA) and Building and Construction Authority (BCA) requirements on new residential developments.

What special considerations apply to property developers and new HDB projects?

The HDB approval process for new Build-To-Order (BTO) projects differs substantially from the resale process. Developers and construction firms operating within HDB’s framework must account for a separate set of procedural requirements, digital submission mandates, and regulatory obligations.

Key distinctions and developer-specific considerations include:

- Digital-only BTO applications: BTO applications are fully digital, with ballot results issued approximately two months after the application window closes. This timeline directly affects project planning and sales forecasting for developers.

- Site and planning approvals: Developers must secure approvals from HDB, URA, BCA, and in some cases the Singapore Civil Defence Force (SCDF) and Public Utilities Board (PUB) before construction commences. Each agency has distinct submission requirements.

- Structural and engineering compliance: HDB mandates compliance with specific structural standards for all new residential developments. Developers must engage qualified Professional Engineers (PEs) for design certification and authority submissions.

- BIM and digital engineering requirements: HDB and BCA increasingly require Building Information Modeling (BIM) submissions for new residential projects. Digital engineering BIM solutions support compliance with these mandates and reduce revision cycles during the approval stage.

- Developer obligations post-approval: Approved developers must adhere to construction timelines, quality benchmarks, and defect liability periods specified in HDB’s development agreements.

Architectural renderings also play a practical role in accelerating project approvals. Visual documentation speeds approvals by giving reviewing authorities a precise reference for design intent, reducing the number of clarification rounds required before sign-off.

Developers who treat HDB compliance as a parallel track to construction planning, rather than a prerequisite, consistently encounter delays at the approval stage. Integrating regulatory submissions into the project program from the outset reduces both timeline risk and cost exposure.

Key takeaways

The HDB approval process requires sequential completion of the HFE letter, resale application, and compliance verification before any residential transaction in Singapore can be finalized.

| Point | Details |

|---|---|

| HFE letter is mandatory first | Obtain the HFE letter before exercising any OTP to avoid transaction delays. |

| 30-day submission deadline | Complete the full HFE application within 30 days of the preliminary check or restart is required. |

| Resale timeline is 8–12 weeks | Plan for 8–12 weeks from OTP exercise to final completion appointment at HDB Hub. |

| Portal validates compliance automatically | HDB’s system cross-checks MOP, ABSD, CPF, and ownership records without manual review. |

| BTO and resale processes differ | Developers must account for digital ballot timelines, BIM requirements, and multi-agency approvals for new builds. |

What experience with the HDB process actually reveals

Having worked extensively with property developers and individual buyers navigating Singapore’s public housing regulatory framework, I have observed a consistent pattern: most delays are self-inflicted and entirely preventable.

The HFE letter is where the majority of timeline failures originate. Applicants treat the preliminary assessment as sufficient confirmation and proceed to schedule viewings, negotiate prices, and sometimes sign letters of intent before the full HFE application is even submitted. When the 30-day window closes and the process restarts, the downstream consequences are significant. Sellers lose confidence. Agents lose patience. Transactions collapse.

The second pressure point I see repeatedly is the coordinated submission requirement for resale applications. Both buyer and seller must submit within 7 days of each other. When one party’s solicitor is slow to act or documentation is incomplete, the other party’s submission sits idle and the clock runs. Appointing solicitors early and confirming their availability before the OTP is exercised is not a formality. It is a risk management decision.

For developers, the most underestimated factor is the multi-agency approval sequence. HDB approval does not exist in isolation. URA, BCA, SCDF, and PUB each have their own submission windows and review periods. Treating these as sequential rather than parallel processes adds months to a project timeline unnecessarily. Integrated engineering consultancy that manages these submissions concurrently is not a luxury for large developers. It is standard practice for any project that needs to stay on schedule.

The digital portals are well-designed and reliable. The process itself is logical. The failures almost always come from inadequate preparation, not from the system.

— Aman

How Com supports HDB project approvals and compliance

Com, operating as Aman Engineering Consultancy, provides integrated engineering and architectural services specifically designed to support HDB project approvals and regulatory compliance in Singapore. From civil and structural design to BIM submissions and multi-agency authority approvals, Com manages the full technical compliance workflow for both individual property owners and large-scale residential developers.

Whether you are preparing documentation for a resale transaction, managing a new BTO development, or coordinating approvals across HDB, BCA, URA, and SCDF, Com’s consultancy team delivers the technical and regulatory expertise required to keep your project on schedule. Visit Aman Engineering Consultancy to discuss your project requirements and receive tailored guidance on the approval process.

FAQ

What is the HFE letter in the HDB process?

The HDB Flat Eligibility (HFE) letter is a mandatory document that confirms a buyer’s eligibility to purchase an HDB flat, their maximum HDB loan amount, and applicable CPF housing grants. It must be obtained before exercising any Option to Purchase.

How long does HDB resale approval take?

HDB resale approval is typically granted within 2 weeks after both parties complete document endorsement and fee payments. The total process from OTP exercise to final completion spans 8–12 weeks.

What happens if the HFE letter expires before purchase?

If the HFE letter expires before the OTP is exercised, the buyer must reapply through the HDB Flat Portal and wait another 21 working days for processing. This delay can jeopardize the transaction if the seller is unwilling to extend the OTP.

How do BTO approvals differ from resale approvals?

BTO applications are fully digital and involve a ballot system, with results issued approximately two months after the application window closes. Unlike resale transactions, BTO approvals also require multi-agency site and construction compliance checks before development commences.

What documents are required for the HDB resale application?

The resale application requires both buyer and seller to submit identity documents, the signed OTP, CPF withdrawal forms, and financial declarations through the HDB Resale Portal. Both parties must complete their submissions within 7 days of each other for the application to proceed.

Recommended

- From Sketch to Approval: A Realistic Timeline for BCA Building Plan Clearance in 2026 – Aman Engineering Consultancy

- HDB Window Replacement: Why You Need BCA Approved Contractors – Aman Engineering Consultancy

- HDB Bathroom Floor Hacking Restrictions The 3-Year Rule – Aman Engineering Consultancy

- HDB renovation permits: What you need for compliance