Accurate building valuation in Singapore determines far more than a number on an appraisal report. It directly controls how much a bank will lend, how much cash a buyer must bring to settlement, and whether a development project pencils out financially. One of the most consequential misconceptions in the local market is the assumption that a bank will simply lend against the agreed purchase price. In practice, banks lend on the lower of the purchase price or the certified market value, a principle that has blindsided experienced investors when valuations returned below the contracted figure. Understanding every dimension of the valuation process is not optional for developers and investors operating in this market.

Table of Contents

- Understanding the core building valuation methods in Singapore

- Navigating regulatory standards and lender requirements in property valuation

- Separating valuation for taxation: Understanding IRAS annual value assessments

- Valuation nuances for commercial and development properties in Singapore

- Practical strategies to manage valuation timing and evidence for successful property deals

- Rethinking valuation: Why developers must treat valuation as a strategic asset, not just a formality

- How Aman Engineering supports your building valuation and development journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Lower-of rule critical | Banks base loans on the lower of purchase price or valuation, affecting cash needed at closing. |

| Valuation methods vary | Methods like comparable sales or income capitalization depend on property type and data availability. |

| IRAS Annual Value differs | Property tax uses estimated rental value, not the market sale value or loan valuation. |

| Timing saves money | Request bank valuations promptly after Option to Purchase to avoid financing surprises. |

| Valuation is strategic | Treat valuation as a deal tool, not just a formality, to optimize purchase and development outcomes. |

Understanding the core building valuation methods in Singapore

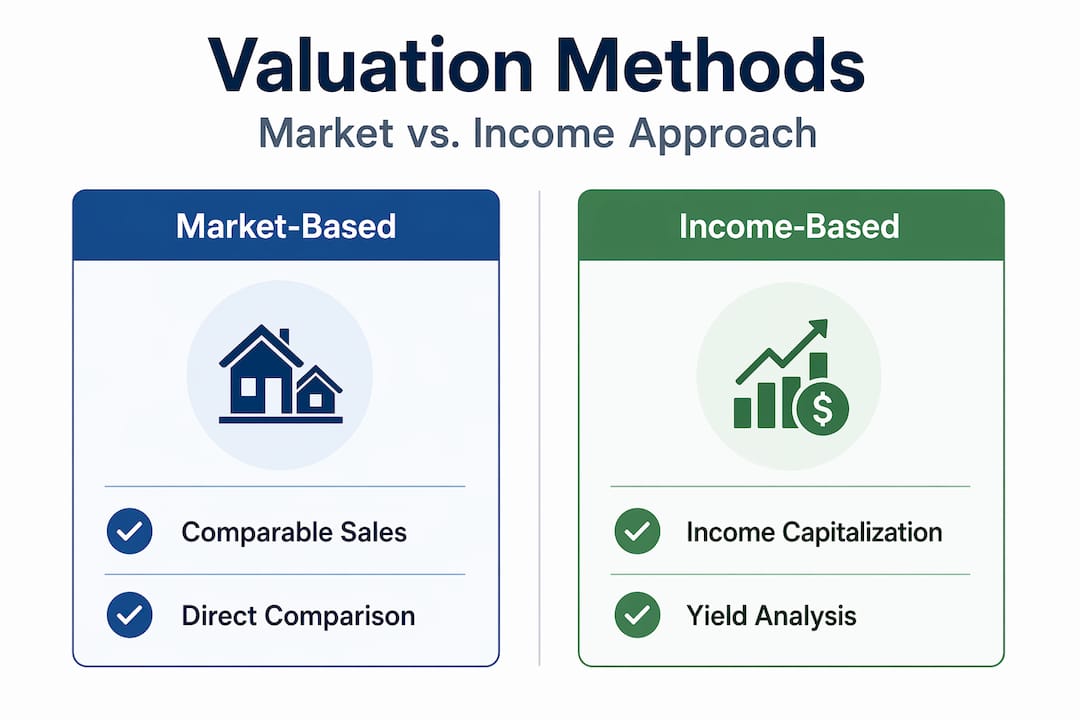

Building on the importance of valuation, the primary methodologies used in Singapore to establish building value with accuracy fall into three recognized approaches. Singapore valuers apply three main approaches depending on property type: comparable sales, income capitalization, and replacement cost. Each method suits a distinct asset class and data environment, and selecting the wrong one produces a figure that lenders, courts, or tax authorities may reject.

Comparable sales method

The comparable sales method, also called the direct comparison approach, is the dominant methodology for residential property appraisal in Singapore. Valuers identify recently transacted properties with similar tenure, floor area, floor level, and location, then apply adjustments for differences. For HDB resale flats, transaction data from HDB’s resale portal provides a dense dataset. For private condominiums, caveats lodged with the Singapore Land Authority serve as the primary evidence base. The method’s reliability is directly proportional to the volume and recency of comparable transactions available.

Income capitalization approach

The income capitalization approach converts a property’s income-generating capacity into a capital value. A valuer estimates the net operating income the asset could realistically produce, then divides it by a capitalization rate derived from market evidence. This method is the standard for commercial property valuation, including office buildings, retail malls, and industrial facilities. A shophouse in Tanjong Pagar generating S$120,000 net annual income, capitalized at a 3.0% rate, would yield a valuation of S$4 million. The chosen capitalization rate is critical; a 0.25% movement can shift valuation by hundreds of thousands of dollars.

Replacement cost method

The replacement cost approach calculates what it would cost to reconstruct the existing building at today’s material and labor rates, then applies depreciation for age, obsolescence, and condition. This method is applied most frequently to specialized properties, such as purpose-built industrial plants, schools, or new-build structures where comparable sales data is sparse. It is also used alongside the other two methods in valuing buildings methodology where structural data supports a precise cost model.

Method selection summary

| Property type | Primary method | Secondary method |

|---|---|---|

| HDB resale flat | Comparable sales | N/A |

| Private residential | Comparable sales | Replacement cost (new builds) |

| Commercial office/retail | Income capitalization | Comparable sales |

| Industrial/specialized | Replacement cost | Income capitalization |

| Development land | Residual land value | Comparable sales |

Key factors that determine method selection:

- Volume and recency of available transaction data

- Whether the property generates measurable rental income

- Asset age and condition relative to market comparables

- Regulatory planning context, including gross floor area and zoning

Pro Tip: When commissioning a real estate valuation Singapore report for a mixed-use development, request that the valuer explicitly state which method was applied to each component and why. A single-method report for a mixed-use asset is often insufficient for lender scrutiny.

Navigating regulatory standards and lender requirements in property valuation

With valuation methods understood, it is equally important to comprehend the regulatory and lending frameworks that govern valuation acceptance and timing. Lenders in Singapore do not accept valuations from any registered firm. Banks require valuations prepared by Monetary Authority of Singapore (MAS)-licensed valuers, and they lend on the lower of purchase price or certified market value. This rule directly affects Loan-to-Value (LTV) ratio calculations, meaning a buyer paying S$2.5 million for a property valued at S$2.3 million must fund the S$200,000 gap entirely from personal resources, in addition to the standard down payment.

MAS licensing and valuer credibility

The MAS maintains oversight of valuers operating within the regulated mortgage lending environment. Valuers must hold an accreditation recognized by the Singapore Institute of Surveyors and Valuers (SISV) or an equivalent body, and the appointing bank typically selects from its own approved panel. Developers and investors working with non-panel valuers for internal feasibility purposes must understand that such reports will not satisfy bank submission requirements, even if the methodology is sound.

Timing, cost, and deal sequencing

Bank valuations typically cost S$300 to S$700 plus GST and take 5 to 10 working days after the Option to Purchase (OTP) is signed. This timeline carries significant implications for deal sequencing. The standard OTP in Singapore grants a 14-day exercise window, which means a valuation requested on day one of the OTP period may return on day 8 or later, leaving minimal time to respond to a shortfall before the option lapses.

Critical regulatory and process considerations:

- Only MAS-panel valuers produce reports acceptable to local lenders

- Cash Over Valuation (COV) on HDB resale flats must be paid entirely in cash, with no CPF or loan coverage

- Valuation reports have an expiry; most lenders require reports dated within three months of loan drawdown

- For commercial property valuation, some banks require two independent valuations for loans exceeding certain thresholds

Engaging a construction compliance checklist framework early in a project cycle helps developers identify valuation-critical regulatory conditions before financing is sought, reducing late-stage surprises.

Pro Tip: For HDB resale transactions where COV is anticipated, calculate the maximum acceptable COV before submitting a bid. COV cannot be financed through any institutional loan product in Singapore, and this is a firm regulatory boundary, not a negotiable term.

Separating valuation for taxation: Understanding IRAS annual value assessments

Beyond transaction and financing valuations, tax-related valuations require distinct understanding to avoid cash flow and compliance mistakes. The Inland Revenue Authority of Singapore (IRAS) uses a separate valuation framework for property tax assessment purposes, and conflating this with market valuation is a common and costly error.

IRAS defines Annual Value as the estimated gross annual rent the property could command if let on the open market, based on comparable market rents, and explicitly excluding furniture, maintenance charges, and any other recoverable expenses. The Annual Value (AV) is not derived from the property’s transactional market value, nor from the actual rent a landlord may be receiving under an existing lease.

Key distinctions between AV and market valuation:

- AV is rent-based; market valuation is capital-based

- AV excludes furniture, fittings, and service charges; market rent may include these

- AV reflects prevailing comparable rents regardless of actual lease terms in place

- AV is reviewed annually by IRAS and adjusted to align with changing rental market conditions

- AV underpins property tax liability, not loan eligibility or sales negotiations

How IRAS derives the Annual Value in practice:

- IRAS collects rental data from comparable properties in the same locality and asset class.

- Gross rent figures are identified from lease agreements lodged with relevant authorities.

- Deductions for furniture, maintenance, and non-structural items are removed from the gross rent figure.

- The resulting net comparable rent is applied to the subject property’s floor area to estimate AV.

- AV is formally assessed and published, with an appeal mechanism available to owners who dispute the figure.

Developers holding properties under long-term leases at below-market rents must be particularly alert. IRAS does not use the contracted rent if it falls materially below current market rates; the authority benchmarks against the open market, potentially producing an AV and therefore a tax liability that exceeds what the actual lease income supports. Feasibility studies valuation work routinely incorporates AV projections to ensure holding cost models remain accurate across the development and asset management cycle.

Valuation nuances for commercial and development properties in Singapore

Having covered tax valuation, we now turn to the specialized valuation factors that shape commercial and development property assessments in Singapore. Commercial assets and development sites involve layers of regulatory and market analysis that residential appraisals typically do not require.

Commercial valuations incorporate market data, income potential, and development considerations, aligning with regulatory requirements and local market nuances that distinguish Singapore from other regional markets.

Leasehold tenure and its valuation impact

Singapore’s land tenure system significantly shapes asset value. Properties on 99-year leasehold land decline in value as the remaining term shortens, with the effect becoming pronounced below 60 years. Banks apply increasingly conservative LTV ratios as leasehold tenure diminishes, and some lenders decline mortgage applications entirely for properties with fewer than 30 years remaining. A freehold commercial property in the same location as a comparable 99-year leasehold asset will consistently command a premium, and valuers model this explicitly in their reports.

Development potential and residual land value

For redevelopment sites, valuers often apply the residual land value method. This approach estimates the completed development’s gross development value (GDV), deducts construction costs, professional fees, financing costs, developer’s profit margin, and all applicable building certification requirements, then derives the maximum supportable land price. The Urban Redevelopment Authority (URA) Master Plan plot ratio and the specific zoning designation are primary inputs because they determine what can be built and at what density.

| Valuation factor | Residential site | Commercial site |

|---|---|---|

| Master Plan plot ratio | Critical input | Critical input |

| Leasehold tenure remaining | High impact | High impact |

| MRT proximity (within 500m) | Moderate positive | Strong positive |

| Gross floor area achievable | Determines GDV | Determines income potential |

| Regulatory planning overlays | May restrict development | May require additional studies |

Factors that materially affect commercial and development property valuation:

- Gross Plot Ratio (GPR) permitted under the current Master Plan cycle

- Conservation status and associated restrictions on modification or demolition

- Proximity to MRT stations, which affects both commercial rental demand and residential desirability

- Traffic Impact Assessments or other regulatory studies required as preconditions to development approval

- JTC or HDB land lease conditions that may restrict use or subletting

Practical strategies to manage valuation timing and evidence for successful property deals

Understanding valuation theory is vital, but applying practical timing and preparation steps is key to deal success. Timing and evidence submitted to the valuer directly influence valuation outcomes and thus the required cash at completion. The following steps address how developers and investors can systematically reduce valuation risk.

Step-by-step approach to managing valuation effectively:

- Commission an indicative or desktop valuation before submitting an offer or signing an OTP. This provides a reference range and prevents committing at a price the bank’s panel valuer is unlikely to support.

- Compile and submit a comprehensive property fact package to the appointed valuer. This includes floor plans, recent comparable transactions, tenancy schedules, and any capital expenditure records that support the condition and income narrative.

- Submit the bank’s valuation request on the first day of the OTP period, not after internal deliberation. The 5 to 10 working day turnaround must fit within the OTP exercise window.

- Pre-calculate the maximum COV or valuation shortfall you can absorb from liquid funds without disrupting project cash flow. Having this figure established before signing prevents reactive decision-making under time pressure.

- For commercial assets, engage a project management in construction framework to ensure that capital improvement works are documented and inspectable at the time of valuation, as valuers assess condition as observed, not as planned.

Pro Tip: Provide the bank’s valuer with a curated comparable transaction schedule, not just the general property information. Valuers are required to substantiate their conclusions with evidence, and pre-assembled, accurate comparables reduce the risk of the valuer defaulting to conservative lower-bound figures.

Rethinking valuation: Why developers must treat valuation as a strategic asset, not just a formality

In practice, building valuation in Singapore is frequently treated as a procedural requirement rather than a strategic instrument. This is a costly perspective. Developers who engage with valuation only after an OTP is signed have already constrained their options. The valuation process hinges on what the appointed valuer can substantiate through inspections and evidence; mismatches between price and certified value lead directly to cash shortfalls that disrupt deal structures.

The more instructive framing is this: valuation is a narrative exercise as much as a technical one. Valuers operate within defined methodological frameworks, but the evidence they receive, the development potential narrative they are presented with, and the comparable data included in the submission all influence the final figure within the defensible range. Developers who present a complete, well-ordered picture of the asset’s income capacity, regulatory potential, and condition support produce more favorable outcomes than those who submit minimal information and await the result.

There is also a structural opportunity that many developers miss. Commissioning a feasibility studies insights assessment that models optimized development scenarios under the current URA Master Plan can directly inform what a valuer concludes about residual land value. If the feasibility work identifies an underutilized plot ratio or a permitted change of use, that information belongs in the valuation brief. A valuer who is unaware of development optionality will almost certainly not factor it into the report.

The professionals who achieve the best financing outcomes in Singapore’s real estate market are those who treat the valuation appointment as a structured submission process rather than a passive event. Evidence quality, timing discipline, and proactive engagement with the regulatory planning context are the instruments through which valuation outcomes are shaped.

How Aman Engineering supports your building valuation and development journey

Navigating building valuation in Singapore requires more than a competent valuer. It requires engineering, compliance, and documentation expertise that supports and validates the valuation narrative across the full project lifecycle.

Aman Engineering Consultancy provides value engineering services that optimize construction cost and design efficiency, directly supporting the financial assumptions underpinning development valuations. Our licensed engineers maintain full professional engineering compliance across BCA, URA, JTC, and other regulatory agencies, ensuring that structural, facade, and M&E documentation meets the standards lenders and valuers require. For developers and investors seeking precision in asset representation, our 3D BIM modeling services produce accurate building data models that support both valuation submissions and regulatory approvals. From feasibility through certification, Aman Engineering provides the technical depth to protect and maximize your asset’s assessed value.

Frequently asked questions

Why do banks in Singapore lend based on the lower of purchase price or valuation?

Singapore banks apply the lower-of rule to protect against inflated purchase prices and ensure loan amounts reflect conservative, independently certified market value rather than a negotiated transaction figure.

How long does a typical formal bank valuation take for private residential properties?

Formal bank valuations for private residential properties typically take 5 to 10 working days after the Option to Purchase is signed and cost between S$300 and S$700 plus GST.

What is the difference between IRAS Annual Value and market valuation?

IRAS Annual Value estimates the gross annual rent a property could achieve based on comparable market rents, and is used solely for property tax assessment, while market valuation reflects capital value for sales and financing purposes.

Can renovation costs fully increase a property’s valuation?

No. Quality renovations typically raise valuation by 2% to 5% above the base property value, not dollar-for-dollar with total renovation expenditure, because valuers assess market evidence, not actual cost inputs.

Why is timing important when requesting a valuation after signing the Option to Purchase?

Requesting a bank valuation immediately after OTP signing ensures the report returns within the 14-day exercise window. Delayed requests risk the valuation arriving after the option has lapsed, forcing buyers to exercise without knowing whether a cash shortfall exists.