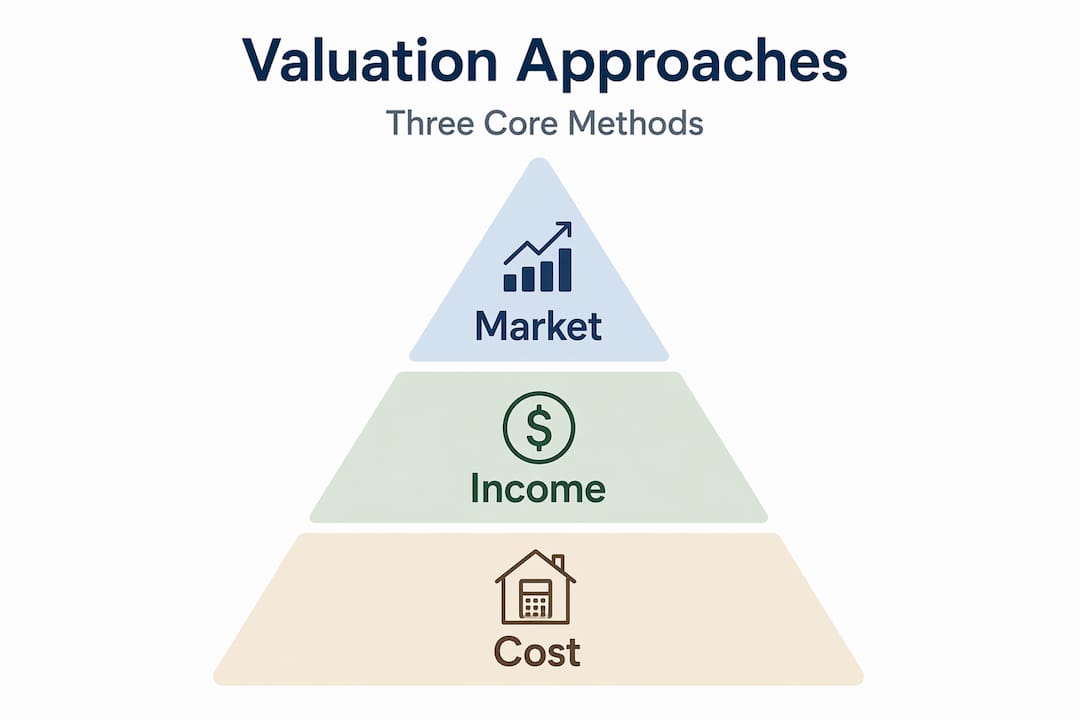

Building valuation methods explained poorly cost real estate professionals money. The core misconception is that one approach fits every property type, whether a single-family home in a residential district, a commercial office tower, or a purpose-built industrial facility. In practice, building valuation relies on three distinct approaches aligned to property type and investor objectives: the market approach, the income approach, and the cost approach. Selecting the wrong method for a given property or transaction can lead to mispricing, failed negotiations, and significant financial exposure. This guide clarifies each method with precision, practical examples, and professional context.

Table of Contents

- Key takeaways

- Building valuation methods explained: the three core approaches

- The market approach: comparables, adjustments, and data quality

- The income approach: capitalization rate and discounted cash flow models

- The cost approach: replacement cost, depreciation, and land value

- Selecting the right approach for your property and goals

- My perspective on judgment, data, and where valuations go wrong

- How Aman Engineering supports accurate building valuation

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Three core valuation approaches | Market, income, and cost approaches each serve distinct property types and investor objectives. |

| Method selection drives accuracy | Applying the wrong approach to a property type produces unreliable value estimates and financial risk. |

| Income approach suits commercial assets | Capitalization rate and DCF models quantify value from projected income streams for leased properties. |

| Cost approach fits unique buildings | Special-purpose properties with no comparable sales require cost-based estimation adjusted for depreciation. |

| Professional judgment is non-negotiable | Final appraisal value reflects weighted professional judgment, not a mechanical average of all three outputs. |

Building valuation methods explained: the three core approaches

Professional valuers do not select a method arbitrarily. Valuers follow a structured hierarchy: first selecting the approach, then the method within that approach, then the quantitative model that converts inputs into a value output. This hierarchy must be disclosed in formal valuation reports under current RICS guidance, providing transparency and reproducibility.

The three recognized approaches are as follows:

Market approach (Sales comparison): Derives value by comparing the subject property to recent sales of similar properties. Best suited for residential properties and any asset class with an active comparable sales market.

Income approach: Derives value from the income-generating capacity of the property. Best suited for commercial, retail, and industrial properties with established tenancy structures and rental income histories.

Cost approach: Derives value by estimating the cost to replace or reproduce the building, then subtracting depreciation, and adding land value. Best suited for new construction, special-purpose buildings, or properties with limited comparable sales data.

| Approach | Primary use case | Key data inputs | Main limitation |

|---|---|---|---|

| Market (sales comparison) | Residential, standard commercial | Recent comparable sales, adjustments | Requires active market with sufficient comps |

| Income (capitalization/DCF) | Leased commercial, industrial, retail | NOI, cap rate, rental data, discount rate | Sensitive to income and expense projection accuracy |

| Cost | New build, special-purpose, unique assets | Replacement cost, depreciation, land value | Depreciation estimation is subjective for aged properties |

Pro Tip: When a property has characteristics that span multiple approaches, for example a mixed-use building that generates income but also has recent comparable sales, request that the appraiser prepare estimates under at least two approaches and explain the weighting rationale in writing.

The market approach: comparables, adjustments, and data quality

The market approach operates on the principle of substitution. A rational buyer will not pay more for a property than the cost of acquiring an equivalent one. The appraiser identifies recently transacted properties with similar characteristics, then applies quantitative adjustments to account for differences in size, location, condition, age, and features.

Selecting the right comparables is the most consequential step. Appraisers prioritize sales within the past six to twelve months, within the same submarket or zoning classification, and with similar gross floor area, construction type, and use designation. Each departure from these parameters introduces adjustment uncertainty.

Key adjustment factors include:

- Location adjustments: Proximity to transit, flood zone classification, and view premiums are quantified using paired sales analysis.

- Condition and maintenance: Property condition and upgrades directly affect perceived value; updated mechanical systems, recent renovations, and structural integrity signals all influence the appraiser’s judgment.

- Gross floor area consistency: Measurement inconsistencies produce valuation gaps of 6 to 15%, and standard protocols often exclude finished basements or attic space even when those areas are regularly occupied.

- Market conditions: Sales older than six months in a volatile market require time adjustments to reflect current pricing levels.

A practical example: if Comparable A sold at $1,200 per square foot but includes a rooftop terrace the subject property lacks, the appraiser applies a downward adjustment to Comparable A’s price before using it as a reference. These adjustments must be supported by market evidence, not estimation.

Pro Tip: When reviewing an appraisal report relying on the market approach, check the adjustment grid carefully. Excessive net adjustments, typically above 15%, or gross adjustments above 25%, signal that the comparable is not truly similar and the value conclusion may be weakened.

The market approach works well in active residential markets but becomes unreliable when transaction volume is low, when market volatility is high, or when the subject property has unique characteristics that limit the pool of true comparables.

The income approach: capitalization rate and discounted cash flow models

For income-producing properties, the income approach uses either implicit capitalization or explicit DCF analysis to estimate capital value. The distinction between these two models matters significantly for commercial and investment-grade assets.

Direct capitalization converts a single year’s stabilized net operating income (NOI) into a value estimate using a market-derived capitalization rate. The formula is straightforward: Property value = NOI divided by cap rate. If a property generates $500,000 in NOI and the market cap rate is 5%, the indicated value is $10 million. The cap rate is derived from recent sales of similar income-producing properties and reflects investor return expectations in that specific market segment.

Discounted cash flow (DCF) analysis projects income and expenses over a defined holding period, typically five to ten years, then discounts those future cash flows to present value using a risk-adjusted discount rate. DCF is the preferred model when income is irregular, when lease expiration profiles create near-term vacancy risk, or when the investor is modeling a specific exit strategy.

| Component | Direct capitalization | DCF analysis |

|---|---|---|

| Income period modeled | Single stabilized year | Multi-year projection (5-10 years) |

| Key rate applied | Capitalization rate | Discount rate and terminal cap rate |

| Best use case | Stable, fully leased assets | Assets with irregular income or lease rollovers |

| Complexity | Lower | Higher |

| Sensitivity to assumptions | Moderate | High |

The income calculation sequence follows a standard structure: start with potential gross income (all rents at full occupancy), subtract vacancy and collection loss to reach effective gross income, then subtract operating expenses to arrive at NOI. That NOI figure feeds directly into the capitalization or DCF model.

For smaller residential investment properties, appraisers sometimes apply the gross rent multiplier as a simplified shortcut: property value divided by gross annual rent. This is less rigorous than full income approach modeling and should not replace a full analysis for significant acquisitions.

Pro Tip: Cap rate sourcing is frequently misunderstood. Cap rates must be derived from actual market transactions of similar properties, not from general market reports or broker opinion. If an appraiser cannot provide transaction evidence supporting the cap rate applied, the income approach conclusion lacks credibility.

The cost approach: replacement cost, depreciation, and land value

The cost approach estimates what it would cost to build an equivalent property today, subtracts accumulated depreciation, and adds the land value. It is the primary approach for special-purpose buildings such as hospitals, schools, places of worship, and government facilities, where comparable sales data is absent and income streams may not apply.

Two distinct cost concepts apply here:

- Reproduction cost: The cost to construct an exact replica of the existing building using the same materials and construction methods. This is rarely used in practice because obsolete materials inflate values for older structures.

- Replacement cost: The cost to construct a building of equivalent utility using modern materials and current construction standards. Replacement cost is generally preferred because it avoids artificially inflating the value of aging buildings through material obsolescence.

Depreciation under the cost approach is classified into three categories:

- Physical deterioration: Wear and tear from age and use, including structural decay, mechanical system degradation, and deferred maintenance.

- Functional obsolescence: Loss in value from outdated design, inefficient floor plans, or systems that no longer meet current standards, such as ceiling heights too low for modern logistics operations.

- External obsolescence: Value loss caused by factors outside the building itself, including adverse zoning changes, environmental contamination in the vicinity, or economic decline in the surrounding area.

Estimating depreciation for older properties is inherently subjective, which reduces the reliability of the cost approach as buildings age. A 40-year-old office building may exhibit functional obsolescence that is difficult to quantify without detailed physical inspection and market demand analysis.

Land value under the cost approach is estimated separately and added to the depreciated cost of improvements. The land is valued at its highest and best use, which may differ from its current use if zoning or market conditions support a more intensive development.

The cost approach overrides other methods when a property is newly constructed, when it is owner-occupied with no income to capitalize, or when the market lacks sufficient comparable sales to support the market approach.

Selecting the right approach for your property and goals

Professional appraisers weigh valuation approaches based on data quality and property fit, not by averaging outputs. The final value conclusion reflects professional judgment about which method best captures the behavior of a typical buyer and seller for that specific property type in that market.

| Property type | Primary approach | Secondary approach |

|---|---|---|

| Single-family residential | Market (sales comparison) | Cost (new construction) |

| Apartment complex | Income (DCF or cap rate) | Market |

| Office / retail | Income | Market |

| Industrial / logistics | Income | Cost |

| Special-purpose (school, hospital) | Cost | Income (if leased) |

| New construction | Cost | Market |

Investor objectives further shape method selection. An investor acquiring a property for income generation needs a defensible income approach analysis to assess yield. An investor pursuing a forced sale or liquidation scenario needs a market approach estimate reflecting current buyer demand. A developer seeking financing for new construction relies primarily on the cost approach to demonstrate replacement value to lenders.

A frequently overlooked issue is the distinction between market value and government-assessed guidance value. Guidance values set by government authorities often diverge significantly from market value, and investors who conflate the two risk incorrect acquisition pricing or unexpected tax liability. A professional valuation always targets a specific defined value type, which must be declared clearly in the report.

Transparency is non-negotiable. Any valuation report should clearly disclose which approach was selected, which method was applied within that approach, and which model was used to quantify the output. Without that disclosure, the conclusion cannot be independently reviewed or challenged.

My perspective on judgment, data, and where valuations go wrong

In my experience working across engineering consultancy and building assessment projects, the most expensive valuation errors are not methodological. They result from poor data inputs and from investors who accept a single number without understanding how it was produced.

I have seen income approach analyses built on speculative lease-up assumptions that bore no relationship to local absorption rates. I have reviewed cost approach estimates where the depreciation adjustment was lifted from a generic table rather than a property-specific physical inspection. Both produce values that look professional but fail under scrutiny.

What I have found actually works is treating the valuation report as a starting point for due diligence, not a conclusion. When the market approach and income approach produce significantly different conclusions, that gap is not a problem to resolve by averaging. It is a signal that something about the property or market requires explanation.

Investors who understand valuation method selection principles are positioned to ask the right questions during acquisition, negotiation, and financing. They recognize when a cap rate is unsupported, when comparable adjustments are excessive, or when a replacement cost estimate is missing an external obsolescence adjustment. That understanding is worth more than the valuation fee itself.

— Aman

How Aman Engineering supports accurate building valuation

Reliable valuation conclusions depend on accurate physical data, including precise measurements, condition assessments, and structural information. Aman Engineering Consultancy provides engineering and consultancy services that directly support the inputs required for defensible building valuations in Singapore and beyond.

Developers, investors, and property owners working with Aman Engineering benefit from value engineering expertise that aligns construction cost analysis with replacement cost valuation requirements. The firm’s inspection, measurement, and compliance services address the data accuracy gaps that consistently undermine valuation reliability. Explore the full range of engineering consultancy services to understand how professional building assessment supports informed investment and asset management decisions.

FAQ

What are the three main building valuation methods?

The three core property valuation methods are the market (sales comparison) approach, the income approach, and the cost approach. Each is selected based on property type, available data, and the purpose of the valuation.

When should the income approach be used?

The income approach is most appropriate for commercial, retail, and industrial properties that generate rental income. It uses either direct capitalization or discounted cash flow analysis to convert projected income into a capital value estimate.

What is the difference between replacement cost and reproduction cost?

Replacement cost estimates what it would cost to construct a building of equivalent utility using modern materials, while reproduction cost estimates an exact replica using original materials. Replacement cost is preferred in current practice to avoid inflating values for older buildings.

How does depreciation affect cost approach valuation?

Depreciation under the cost approach is classified as physical deterioration, functional obsolescence, or external obsolescence. Estimating these categories for older properties involves significant professional judgment and reduces the reliability of this method as buildings age.

Why do appraisers use multiple valuation approaches?

Appraisers develop value indications under multiple approaches when data supports it, then weight those conclusions based on property type and data quality. The final value is a professional judgment call, not a mathematical average of all three outputs.